Hover over any term that is underlined with a dotted line to read its definition.

Subscribe on Google | Apple Podcasts | Spotify | Amazon

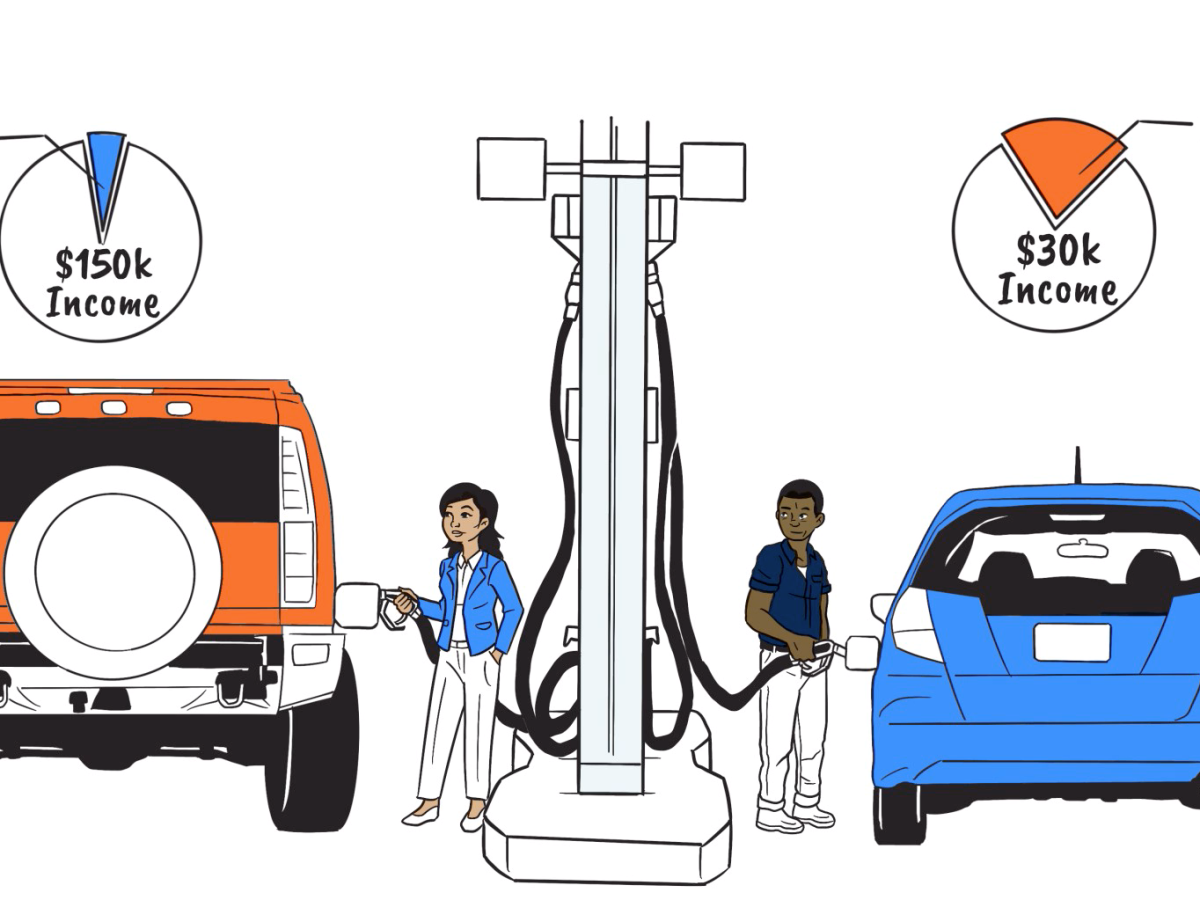

In rural Abita Springs, Louisiana, it’s nearly impossible to get anywhere by foot. Driving is a means of survival.

Jacques LeBourgeois, 66, understands this better than most. He lost his driver’s license because of a tax debt to the state.

“I get a letter in the mail, saying, ‘Your license was revoked,’” said LeBourgeois, who is retired, in ill health and lives alone. “Basically, all your rights have been revoked in the state.”

In Louisiana, the state can take your license for income tax debts — as little as $1,000 — and it’s done so more than 19,000 times this year alone, according to data obtained by the Center for Public Integrity. LeBourgeois’ debt totaled around $10,000, much of that penalties and interest, but it’s been difficult for him to get to the bottom of the original debt that began accruing in 2004.

The Internal Revenue Service might have a fearsome reputation in the public imagination when it comes to income tax debt collection, but most states are far more aggressive, using strategies that hit lower-income residents particularly hard, a Public Integrity investigation found.

At least nine states can suspend or decline to renew driver’s licenses over unpaid taxes. California will only take your license if you owe more than $100,000, but Maryland sets no minimum amount for preventing renewal.

At least 16 states and Washington, D.C., can suspend or decline to renew professional licenses for unpaid tax debt. As with driver’s licenses, that Catch-22 penalty undercuts a taxpayer’s ability to pay up. A 2020 Arizona State University study of such license revocations suggests the consequences largely fall on people in financial distress because of low-wage jobs, rather than willful tax evaders.

The IRS, by comparison, doesn’t revoke professional or driver’s licenses for unpaid federal income tax.

The differences don’t end there. The IRS has a decade to collect federal income tax debt, after which it’s considered forgiven. At least 10 states set longer limits — California and Illinois, for example, can go after state income tax debt twice as old. And at least nine others can pursue state tax debt indefinitely.

The higher the interest rate on the debt, the faster it mounts. As of fall 2023, at least 14 states charged more than the current 8% IRS rate.

And the IRS offers far more assistance for taxpayers in financial hardship than most states, Public Integrity found.

“Unlike the federal government, nearly every state has a constitutional balanced budget requirement,” Anna Gooch with the Center for Taxpayer Rights said in an email. “This means that the state cannot spend more than what it collects. As a result of this limitation, these states are more dependent on tax revenue than the federal government is, and that is reflected in how the states approach tax collection.”

State revenue agencies have discretion over some of their practices. But other times they’re at the mercy of state statutes that dictate how they must collect. In those cases, relief for taxpayers in hardship would require that legislators change the law.

Related story

Tax terms: Here’s what all those confusing phrases mean

To understand collection policies, Public Integrity asked every state with an individual income tax on wages about their rules and interviewed nearly 30 low-income taxpayer clinic attorneys across the country. Some state revenue agencies ignored repeated requests for this basic information.

Across the country, the way states have chosen to tax is helping fuel the country’s stark economic inequality, with poorer residents paying a higher share of their income than richer ones — a disproportionate hit for people of color.

States’ collection practices can make the problem worse.

“A lot of folks feel like it’s just the extra weight on top of them,” said Eric Santos, executive director of the North Georgia Low Income Taxpayer Clinic. The IRS funds such clinics around the country to assist eligible people at low or no cost. “They feel like they’re never going to get out from under it.”

Lack of resources is the key problem — and not only because low-wage jobs and little savings in retirement make it hard to keep up with basic expenses. Low-income people don’t have the money to pay for accountants or other help filing tax returns, Santos said. That makes it harder to navigate a complicated system and increases the odds of honest mistakes that snowball, he said.

“By virtue of these things, a poor person is more likely to end up in collections,” he said. “If they do, you don’t want that system to be excessively brutal.”

Losing your license over tax debt

Brad Keller was trying to find out how much he owed in state taxes, and why. He couldn’t get a straight answer.

Over weeks of calls to the Illinois Department of Revenue last year, one representative told him the problem was wage information missing from his 2020 return. Another said he should have filed returns for 2014 to 2017, even though his income on disability was too low to owe anything. Yet another said he owed taxes from both 2013 and 2008.

One Friday night, he came home to seven letters from the agency, each citing different debts ranging from $7,000 to $9,000.

But perhaps the most bewildering part was the one thing the state was clear about: If he didn’t pay up quickly, the state would yank his license to work as a security guard, which he’d just renewed after knee replacements improved his mobility.

“I’m on disability and I want to work a little bit, and if I can’t work, I won’t be able to pay you,” Keller recalls telling an agency representative during one call. “That person said, ‘I don’t care. We’re going to suspend your license.’”

And they did.

States that suspend professional or driver’s licenses for unpaid tax debt see it as a collections tool. But attorneys, experts and those who have had their licenses revoked say the policy drives people facing financial difficulty into even deeper hardship.

A 2020 study from researchers at Arizona State University looked at the suspension of medical licenses in Missouri for tax debt. Most affected, they found, were the medical professions with the lowest incomes, such as massage therapists and licensed practical nurses.

Nearly 10 percent of LPNs and massage therapists lost their licenses due to unpaid taxes over an eight-year period the study examined.

In an interview, authors David Kenchington and Roger White said license-suspension policies are based on the assumption that any nonpayment is an intentional choice, and severe penalties can change that behavior. “What we were trying to get at with this paper was, ‘Well, what if there was a group of people that just can’t afford to pay?’” Kenchington said.

Their findings suggest that’s exactly what is happening.

“It is unlikely that so many of these workers make a choice to give up their professional license to avoid a tax bill that is relatively paltry (on the order of a few hundred dollars), as they were very recently willing to expend the time and money necessary to apply for or renew said professional license,” they wrote in the study.

Missouri’s Department of Revenue, which handles tax collection for the state that study focused on, did not respond to multiple requests for information about or comment on its policies.

The Illinois Department of Financial and Professional Regulation, which suspended Keller’s license, said it had no discretion under state law to do otherwise. The Department of Revenue, which notified the agency of the tax debt, said it “does provide payment plan options for those who cannot pay their bills in full.”

The revenue agency added that it “strives to make the tax process as easy as possible for taxpayers and works closely with those trying to resolve delinquent tax matters.” Though it did not comment on Keller’s case, it said that notices showing different delinquent tax amounts are most likely due to mounting penalties and interest.

Arizona State University’s Kenchington and White were trying to fill a gap in tax research. But theirs is not the only study that found financial struggles at the heart of unpaid taxes.

In 1997, Arkansas forgave all interest and penalties to delinquent taxpayers who applied for a temporary tax amnesty program. A 2003 paper found the average income of participants who admitted to not paying their taxes was about $36,000, and the typical person owed about $500.

One of the most common reasons they gave: “lack of money.”

Public Integrity asked several states for data on tax debts broken down by income, ZIP code, amount owed and enforcement action to shed more light on collections practices and who they affect most. A year later, the revenue agencies in Louisiana, New Jersey and New York have yet to provide that.

Related story

How state taxes make inequality worse

New Jersey said it would charge $9,760 for the data, then increased the figure to $15,250 and stopped responding as Public Integrity journalists tried to negotiate to get portions of the data at a lower cost.

Oregon’s Department of Revenue shared some data about past-due taxes owed by individuals and businesses as of June 2022. Those who owed less than $1,000 at that time accounted for nearly half of delinquent taxpayers but only 2.6% of the money the agency was trying to collect.

Separate data the state shared for 2019 and 2020 revealed that Oregonians with incomes between $33,000 and $58,000 had the highest rates of tax delinquency.

And that’s a state that leans less heavily on its lowest-income residents in how it taxes, compared with most of the country.

Unlike private debt collectors, state governments have a vested interest in the wellbeing of residents. That’s one reason to consider hardship when taxes are overdue.

Send us tips

Have you had issues with tax collections? We want to hear about it. Email msrikrishnan@publicintegrity.org.

Another is simply pragmatic.

“If a taxpayer loses their job because they can no longer legally drive to work, how is this going to enable them to pay their tax debt?” asked Gooch, with the Center for Taxpayer Rights. “It’s not.”

New York, which will yank driver’s licenses once tax debt reaches $10,000, passed a law in 2019 that added adjustments for inflation and hardship exemptions to its suspension process. Fordham University law students who pressed for the hardship change found that tens of thousands of New Yorkers received notices from 2014 to 2017 that their licenses would be suspended over tax debt.

A similar legislative effort in Maryland failed to pass.

The 2019 bill would have prohibited the state from denying vehicle registration or driver’s license renewals for people in financial hardship or whose tax debt is below $10,000, not including interest and penalties.

The state Department of Legislative Services and the Comptroller’s Office said in an analysis that 90% of cases now eligible for these collection tactics would likely be exempted under the legislation. They estimated the resulting reduction to state revenue at about $239 million over a five-year period — offering some idea of how much money the state may be collecting from people in financial distress.

“If a taxpayer loses their job because they can no longer legally drive to work, how is this going to enable them to pay their tax debt? It’s not.”

Anna Gooch with the Center for Taxpayer Rights

While the unpaid tax debts are likely significant for many who owe them, the amount collected annually averages less than one-half of one percent of the state’s general fund budget.

Asked in Public Integrity’s survey about the license non-renewal policy, the Maryland Comptroller’s Office said, “Our office is always willing to work with taxpayers to have their income tax debt issues resolved in a reasonable and timely manner to avoid this outcome.”

In a later statement, the office said it’s helped 102 taxpayers with hardship cases so far in 2023, in addition to hundreds of cases its compliance team members “have handled through other programs and in the regular course of business.”

Louisiana suspended nearly 14,000 licenses for tax debt in 2018, according to a report from advocacy organization Louisiana Appleseed. In the five years that followed, the state suspended nearly 39,000 licenses for the same reason, according to data obtained by Public Integrity. The state paused license suspensions during the COVID-19 pandemic, or the number likely would have been higher.

Paul Tuttle, director of the Low Income Taxpayer Clinic at Southeast Louisiana Legal Services, said he sees this situation with his clients all the time.

“I’ve had people who are truck drivers come to me and say, ‘I owe the state tax liability and I drive a truck for a living and they suspended my commercial license and now I can’t work, I can’t make any money, how do they expect me to pay them back if they take away my livelihood?’” Tuttle said. “In rural areas, people need a car just to drive to work and grocery shopping and things like that. So it’s like a really critical thing that people need to take away from them.”

The Louisiana Department of Revenue said the agency does not track license suspensions by income range to analyze the impact on lower-income people.

“We are currently working on solutions to resolve issues raised related to drivers license suspensions,” the agency wrote in an email.

‘They’re taking all my money’

In February, the state of Virginia drained Mohammed Siddique’s bank account.

There was only $42 in there, he said, a symptom of his family’s tight finances. Then Siddique received a letter that the state was going to start taking his paychecks in their entirety.

Virginia said Siddique owed them more than $41,000 because he didn’t pay what he was supposed to in taxes more than a decade ago. Siddique believes that’s inaccurate, but he — like many — hasn’t saved his tax returns from that long ago. And he can’t afford to pay the debt.

“For days, I didn’t sleep because they’re taking all my money, so how can I pay the rent and all these things?” asked Siddique, who has two children.

He works as a cashier at Macy’s. Depending on the hours he gets, he makes between $1,600 and $1,800 a month. His wife works one to two days a week and the loss of his paychecks meant they were dependent on her income, even more limited than his.

He sent countless letters and spent hours on the phone trying to tell Virginia’s Department of Taxation and the private collections agency it contracted with that he could not afford to pay the debt.

In June the state began to siphon money from Siddique’s wages. First, they took an entire paycheck. For the next two, after he emphasized again that he was experiencing financial hardship, they took 25%.

None of that was allowed, said Nancy Ryan, director of the Low Income Taxpayer Clinic for Legal Services of Northern Virginia and an attorney who has taken on Siddique’s case. In Virginia, the state must leave you a minimum amount per paycheck to support your family. Siddique’s wages usually don’t surpass that amount.

“Imagine just not getting your paycheck one or two times,” Ryan said. “We work with low-income people and that can be devastating. They miss their rent and get evicted or they miss a car payment and their car gets taken and then they can’t get to work.”

Virginia’s Department of Taxation declined to comment on Siddique’s case.

Simply getting details about collections rules, meanwhile, is difficult in many states.

“In a few states, information is readily available, and the state is willing to listen to taxpayers and advocates when it comes to making that information more available,” Gooch said. In less transparent states, “it can be difficult for taxpayers and tax professionals to find any information on how the state conducts tax collection.”

Gooch, who is working on a survey of state tax practices, said it’s been particularly difficult for her and volunteer attorneys helping her fill out the survey to find information about hardship policies such as payment plans, debt settlements and temporary pauses on collections. In the states that have those programs, she said, it’s been hard to determine who qualifies.

That’s precisely what Public Integrity found. We asked states for basic information taxpayers need to know: the statute of limitations for collections, whether the states suspend licenses, the circumstances under which a state will initiate a tax lien or wage garnishment, the interest and penalty rates, and options for people experiencing financial hardship.

Of the 41 states and D.C. that have an individual income tax on wages, five failed to answer any of the questions despite repeated reminders by email and telephone.

A spokesperson for New York’s revenue agency offered an explanation that implied routine policies were state secrets: “We typically do not discuss enforcement strategies.”

RElated story

State tax systems contribute to inequality. These states are doubling down.

Of those that answered, many were short on details.

West Virginia’s State Tax Department refused to tell us the minimum time and amount owed before they will initiate a tax lien, levy or wage garnishment, saying it was “confidential information.”

“Disclosure of such information would provide malefactors with a roadmap in furtherance of tax noncompliance,” wrote West Virginia Tax Commissioner Matthew Irby.

Beverly Winstead, director of the University of Maryland’s Low Income Taxpayer Clinic, points out that the IRS’ Internal Revenue Manual lays out its procedures clearly and publicly. She wishes Maryland did the same.

On the upside, Maryland provides funding to low-income taxpayer clinics to help residents with tax issues, one of few states that does so. But the lack of publicly available information is a problem, Winstead said.

“It makes it harder to know your rights and options,” she said. “It also tends to aid in inconsistent answers. If I call the Comptroller’s Office and say, ‘I want to enter a payment plan,’ I may call to speak to one agent and get one answer and speak to another one and get another answer.”

The Maryland Comptroller’s Office said in a statement that it aims for more flexibility so people in hardship who don’t qualify for certain programs still have options.

“To ensure that our agency is better sharing information, we are in the process of completely rebuilding the agency’s website,” the office said in an emailed statement. “Comptroller [Brooke] Lierman has also dedicated resources to creating a public engagement team that reaches out to communities, nonprofits, and others to provide information on agency services. In the coming fiscal year, the agency is looking to expand our capacity and to grow our outreach and capability to help individuals needing our assistance.”

related story

The long struggle over taxing the rich

Compared with how the IRS handles financial hardship, many states’ options are limited.

The federal government will indefinitely pause collections actions against people who can demonstrate they’re unable to pay back their debt. Many states do no such thing.

Attorneys also say it’s typically more straightforward to negotiate settlements with the IRS. Known as an “offer in compromise,” such a settlement reduces the amount of money the taxpayer must come up with.

“The IRS is very reasonable at dealing with lower-income taxpayers who have tax debts,” said Robert Nassau, director of the Low Income Taxpayer Clinic at Syracuse University. “They’re very understanding of people’s circumstances. Compared to the IRS, the New York State Department of [Taxation and] Finance is the devil. The state wants to be a lot more aggressive than the federal government.”

Project team

Reporters: Maya Srikrishnan, Ashley Clarke, Joe Yerardi and Jamie Smith Hopkins

Editors: Jamie Smith Hopkins and Matt DeRienzo

Design: Janeen Jones

Graphics: Joe Yerardi

Partner and audience engagement: Lisa Yanick Litwiller, Ashley Clarke and Vanessa Lee

Fact-checking: Peter Newbatt Smith

Audio: Juliana Marin

Nebraska, for example, can settle debts through an offer in compromise, but there’s no formal application process, according to Legal Aid of Nebraska’s Tax Law Project. “It would be incredibly difficult for a taxpayer without an attorney to apply,” Shailana Dunn-Wall, a lawyer there, said in an email.

Dunn-Wall said her clinic has had such offers accepted by the state only twice in the past five years.

“Most of our clients who are eligible for an [offer] or currently not collectible status with the IRS are not eligible for similar treatment from the Department of Revenue,” Dunn-Wall said.

Nebraska’s Department of Revenue initially declined to answer questions about its policies but ultimately confirmed the Tax Law Project’s summary. Asked how it approaches hardship cases, the agency said by email, “Each person’s situation is reviewed on its own merits.”

Louisiana accepted 24 offers in compromise for individual income tax cases in the fiscal year that ended June 30, 2022, according to its most recent annual tax collection report. Tuttle, with Southeast Louisiana Legal Services, said it’s very difficult to get the state to approve an offer of any amount.

Its payment plans, meanwhile, require a 20% down payment and can be stretched out for only three years. That’s not something Tuttle’s clients can typically do. The IRS, by contrast, requires no down payment and allows twice as long for repayment.

“The attitude of the [Louisiana Department of Revenue] is that ‘they have the money to pay, they just won’t give it, so we have to force them to do it. … We have to twist their arm somehow to get the money,’” Tuttle said. “It never seems to occur to them that maybe the person actually does not have all the money right now to pay them and they need some flexibility and some other options to pay it back.”

‘Absolutely no money’

After Siddique found an attorney at one of Virginia’s low-income taxpayer clinics, the state returned the money it took. He submitted a request for the state to compromise with him: He would pay what he could and the state would settle his debt.

“I offered them $100 because I can’t afford to pay anything more,” Siddique said.

As of November, he was waiting for an answer.

Keller, who lost his license to work as a security guard, was finally able to come to an agreement with Illinois to pay a $2,700 debt in installments and get his license back.

He’s returned to working as a security guard. With the additional income, he said he managed to halve his debt in a matter of months.

For LeBourgeois, the Louisiana resident, it’s been a long struggle.

He worked for years for a catering company, buffeted by the economic downturns the state experienced after Hurricane Katrina, the Great Recession and the BP oil spill. As his paycheck dwindled and his health declined, he fell behind on his state and federal income taxes.

Confusion over tax rules for contractor pay added to his woes. Overwhelmed with bills he knew he could not pay, he reached the point where he would crumple up notices that he received in the mail.

“I couldn’t go back to work,” he said. “I had absolutely no money. I mean, that was it. I was broke. I still am.”

He lives in a small house inherited by his sister, who lets him stay there. He gets a monthly check from Social Security that he stretches to cover necessities. He said the IRS stopped trying to collect from him years ago when he explained his situation, but the state didn’t. It suspended his driver’s license around 2019, he said.

Taxpayers can get a year-long limited “hardship” license in Louisiana, buying a little more time to get money together. But LeBourgeois didn’t have any. It was the early part of the COVID-19 pandemic, to his recollection, when that expired and he had no legal way to drive.

Doctors’ appointments, grocery shopping, prescription pickups — the everyday business of staying alive was suddenly far harder.

“They want their money,” he said of the state in a September interview. “You know what I mean? They don’t care. They just don’t care.”

Asked about his case, the Louisiana Department of Revenue did not respond.

LeBourgeois called the agency repeatedly, but no one offered any alternatives besides paying the full amount, he said. Finally, someone he knew pointed him to Tuttle, the low-income taxpayer clinic attorney.

Tuttle submitted LeBourgeois’ financial documents with an offer that the IRS had already agreed to: settling the debt for $1. It was all he could afford.

They waited.

In early November, the state accepted.

LeBourgeois rushed to get his license back. On Nov. 16, he finally held it in his hands.

The impact of the last several years, he reflected that afternoon, wouldn’t be wiped away like the debt.

“I paid a cost in mental health and physical health,” he said. “It might not have been monetary, but it was definitely a cost.”

Public Integrity journalists Joe Yerardi and Jamie Smith Hopkins contributed to this story.